When we study multiple stock prices together, one of the first questions is: do they move together, and if so, by how much and with what delay? Cross-correlation answers exactly this.

Cross-correlation measures the similarity between two time series as a function of a lag applied to one of them. Unlike a simple correlation coefficient (which is a single number), cross-correlation gives us a function that reveals:

How strongly two stocks co-move

Whether one leads the other (a lag > 0 suggests stock A today predicts stock B tomorrow)

How persistent that relationship is over time

This post covers cross-correlation from first principles, applied to real Korean stock data.

2 Setup

Code

# Install if needed:# pip install FinanceDataReader pandas numpy matplotlib seaborn scipy statsmodelsimport FinanceDataReader as fdrimport pandas as pdimport numpy as npimport matplotlib.pyplot as pltimport matplotlib.dates as mdatesimport seaborn as snsfrom scipy import statsfrom statsmodels.tsa.stattools import ccf as sm_ccffrom statsmodels.tsa.stattools import grangercausalitytestsplt.rcParams['figure.dpi'] =120plt.rcParams['font.size'] =11sns.set_theme(style='whitegrid')

3 1. Downloading Korean Stock Data

We use FinanceDataReader, which supports KOSPI and KOSDAQ natively.

Code

# Major Korean blue-chip stockstickers = {'005930': 'Samsung Electronics','000660': 'SK Hynix','035420': 'NAVER','035720': 'Kakao','005380': 'Hyundai Motor','005490': 'POSCO','105560': 'KB Financial','000270': 'Kia',}start ='2018-01-01'end ='2024-12-31'prices = {}for ticker, name in tickers.items(): df = fdr.DataReader(ticker, start, end) prices[name] = df['Close']prices = pd.DataFrame(prices)prices.index = pd.to_datetime(prices.index)prices = prices.dropna()print(f"Shape: {prices.shape}")print(f"Period: {prices.index[0].date()} to {prices.index[-1].date()}")prices.head()

Shape: (1721, 8)

Period: 2018-01-02 to 2024-12-30

Samsung Electronics

SK Hynix

NAVER

Kakao

Hyundai Motor

POSCO

KB Financial

Kia

Date

2018-01-02

51020

76600

177251

29405

149500

339000

63100

32800

2018-01-03

51620

77700

174447

29906

150500

357500

63100

32600

2018-01-04

51080

77100

178853

31311

146500

367500

63000

31550

2018-01-05

52120

79300

181857

31311

149000

368000

64100

31950

2018-01-08

52020

78200

190269

32014

151000

369500

66600

32400

4 2. Exploratory Data Analysis

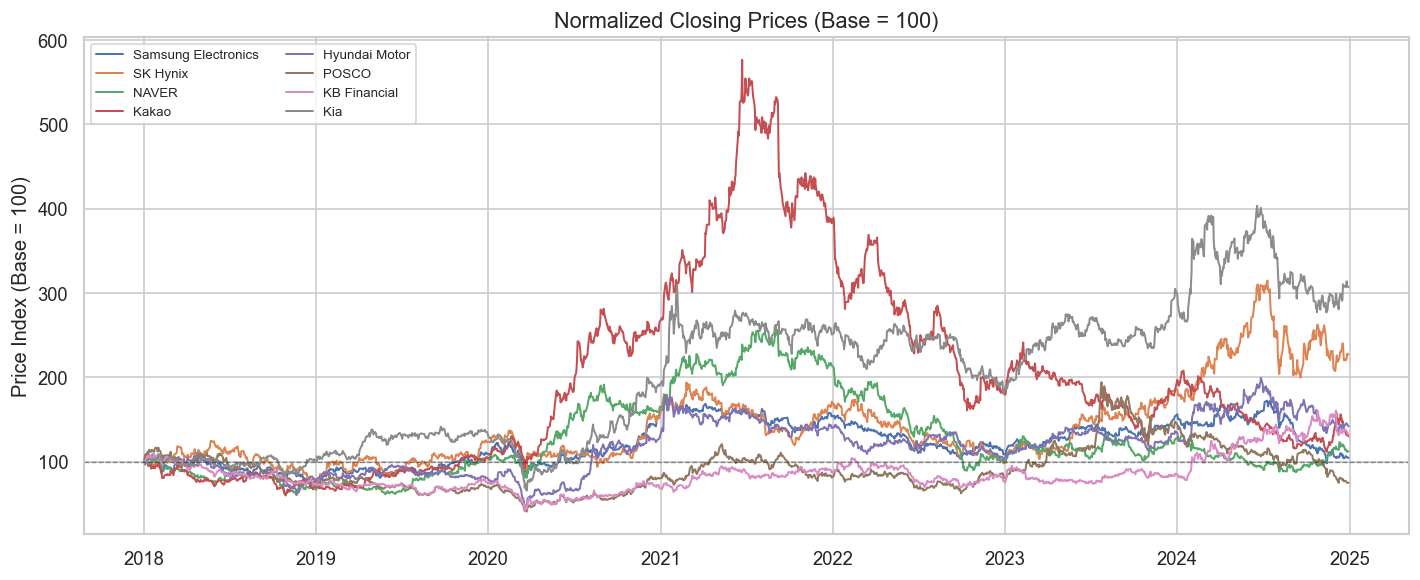

4.1 2.1 Normalized Price Trajectories

Raw prices have very different scales. We normalize to 100 at the start to compare trajectories.

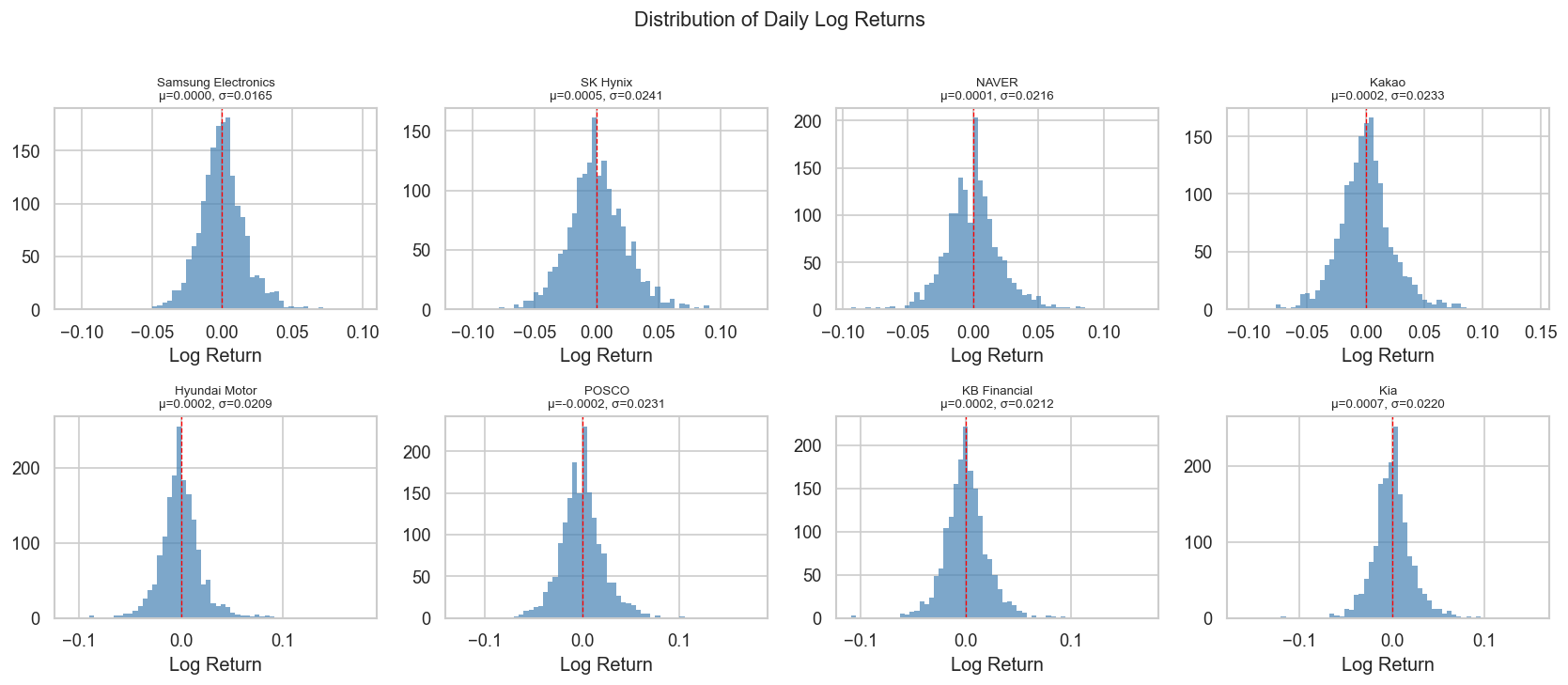

Interpretation note: Stock returns are almost never normal. Excess kurtosis > 0 (“fat tails”) means extreme moves are more common than a normal distribution predicts. The Jarque-Bera test formalizes this: p-value < 0.05 rejects normality.

5 3. Cross-Correlation: Theory

5.1 3.1 Pearson Correlation (Lag = 0)

The familiar correlation coefficient between two return series \(X\) and \(Y\) is:

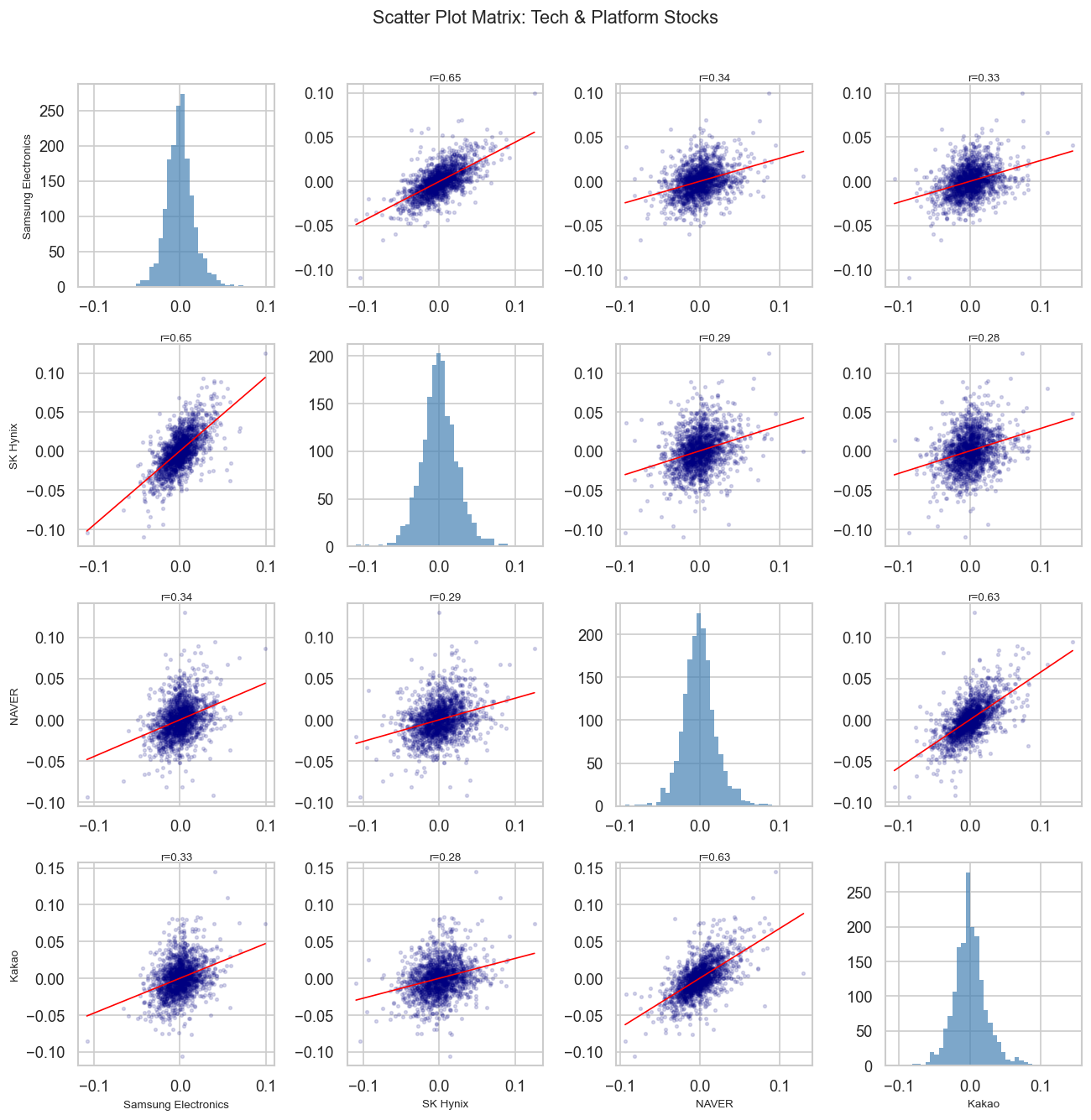

selected = ['Samsung Electronics', 'SK Hynix', 'NAVER', 'Kakao']sub = returns[selected]fig, axes = plt.subplots(4, 4, figsize=(11, 11))for i, col_i inenumerate(selected):for j, col_j inenumerate(selected): ax = axes[i][j]if i == j: ax.hist(sub[col_i], bins=40, color='steelblue', alpha=0.7, edgecolor='none') ax.set_xlabel(col_i if i ==3else'')else: x, y = sub[col_j], sub[col_i] ax.scatter(x, y, alpha=0.15, s=5, color='navy')# regression line m, b, r, p, _ = stats.linregress(x, y) xr = np.linspace(x.min(), x.max(), 100) ax.plot(xr, m * xr + b, color='red', linewidth=1) ax.set_title(f'r={r:.2f}', fontsize=8, pad=2)if j ==0: ax.set_ylabel(col_i, fontsize=8)if i ==3: ax.set_xlabel(col_j, fontsize=8)plt.suptitle('Scatter Plot Matrix: Tech & Platform Stocks', fontsize=13, y=1.01)plt.tight_layout()plt.show()

7 5. Cross-Correlation Function (CCF)

The CCF tells us whether one stock leads or lags another. This is crucial for understanding information flow in markets.

7.1 5.1 CCF for a Single Pair

Code

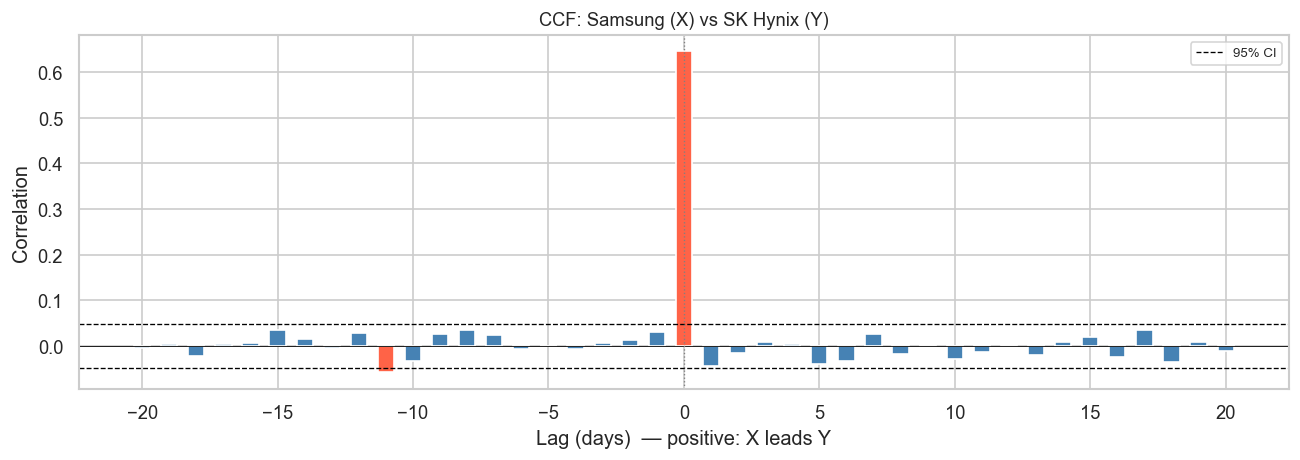

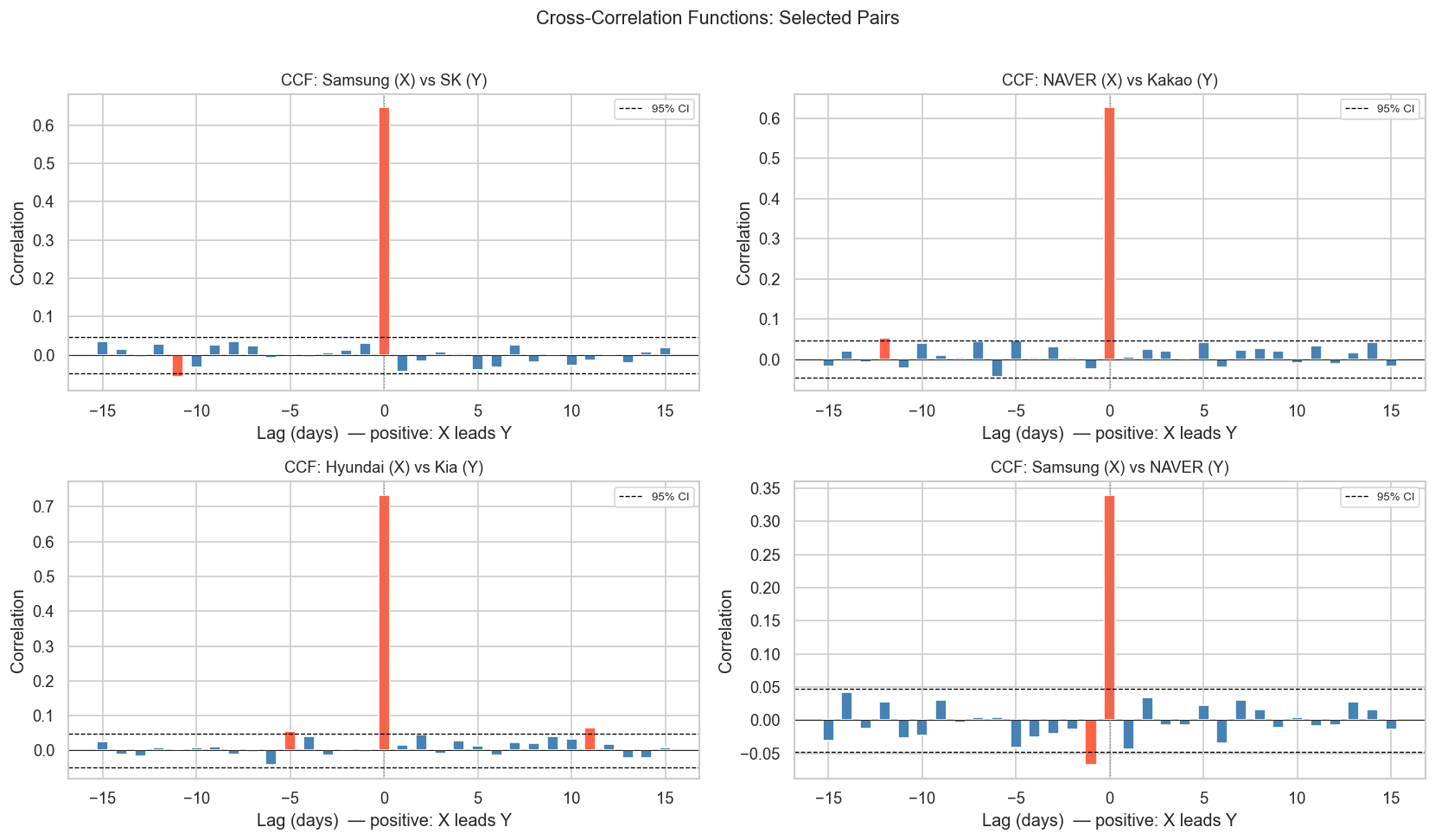

def plot_ccf(x, y, name_x, name_y, max_lag=30, ax=None):"""Plot cross-correlation function with confidence bounds."""if ax isNone: fig, ax = plt.subplots(figsize=(10, 4)) n =len(x) conf =1.96/ np.sqrt(n) lags = np.arange(-max_lag, max_lag +1) ccf_vals = []for lag in lags:if lag ==0: ccf_vals.append(np.corrcoef(x, y)[0, 1])elif lag >0: ccf_vals.append(np.corrcoef(x[:-lag], y[lag:])[0, 1])else: ccf_vals.append(np.corrcoef(x[-lag:], y[:lag])[0, 1]) colors = ['tomato'ifabs(v) > conf else'steelblue'for v in ccf_vals] ax.bar(lags, ccf_vals, color=colors, width=0.6) ax.axhline(conf, color='black', linestyle='--', linewidth=0.8, label='95% CI') ax.axhline(-conf, color='black', linestyle='--', linewidth=0.8) ax.axhline(0, color='black', linewidth=0.5) ax.axvline(0, color='gray', linewidth=0.8, linestyle=':') ax.set_xlabel('Lag (days) — positive: X leads Y') ax.set_ylabel('Correlation') ax.set_title(f'CCF: {name_x} (X) vs {name_y} (Y)', fontsize=11) ax.legend(fontsize=8)return ccf_vals, lagsx = returns['Samsung Electronics'].valuesy = returns['SK Hynix'].valuesfig, ax = plt.subplots(figsize=(11, 4))plot_ccf(x, y, 'Samsung', 'SK Hynix', max_lag=20, ax=ax)plt.tight_layout()plt.show()

Reading the CCF plot: Red bars exceed the 95% confidence band — these lags show statistically significant correlation. A positive lag means Samsung today predicts SK Hynix in lag days.

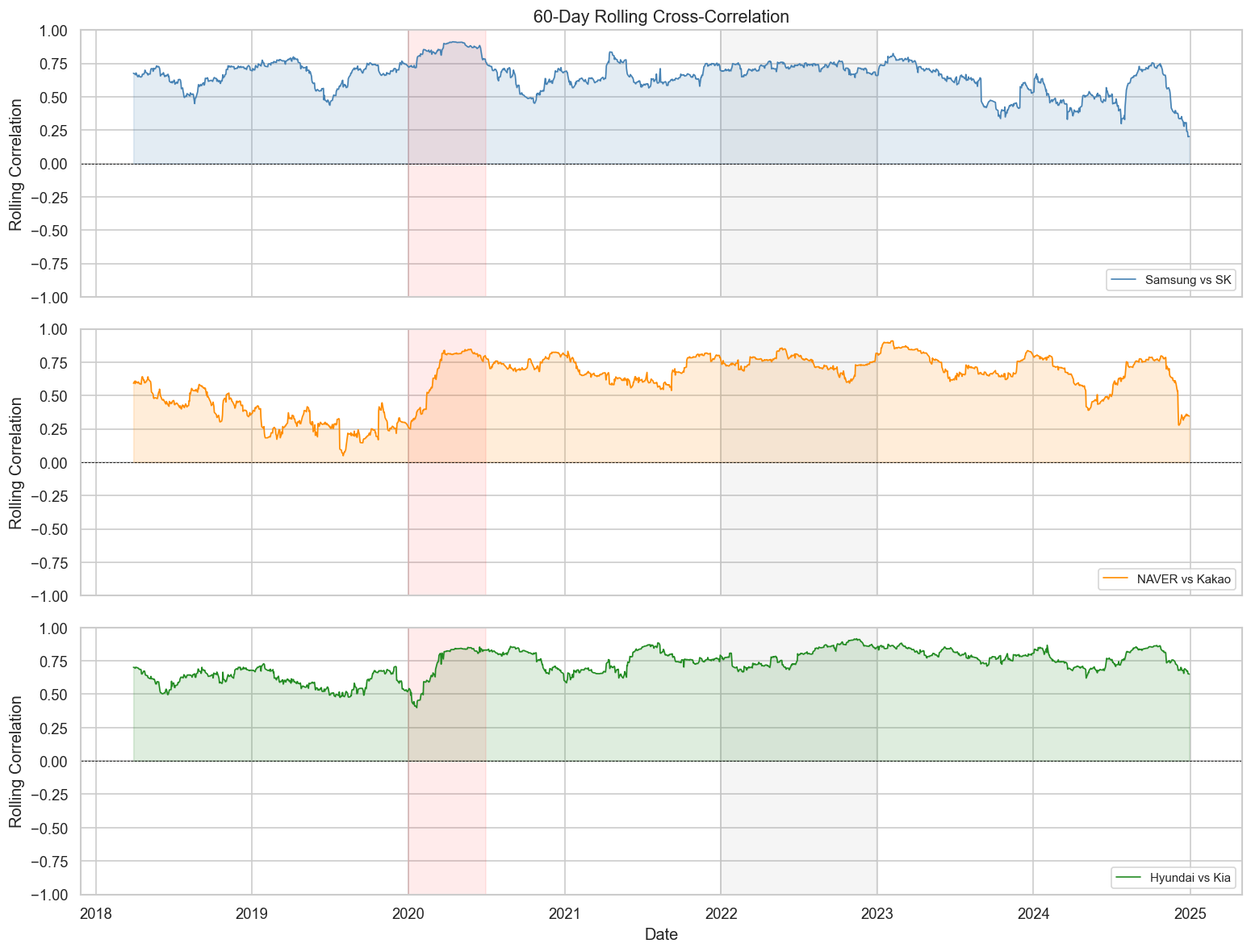

The correlation between stocks is not stable over time — it changes with market regimes (bull, bear, crisis). Rolling correlation captures this dynamics.

Key insight: Correlations spike toward 1.0 during market crises (COVID-19 crash in early 2020). This is the “correlation breakdown” problem — diversification fails precisely when you need it most.

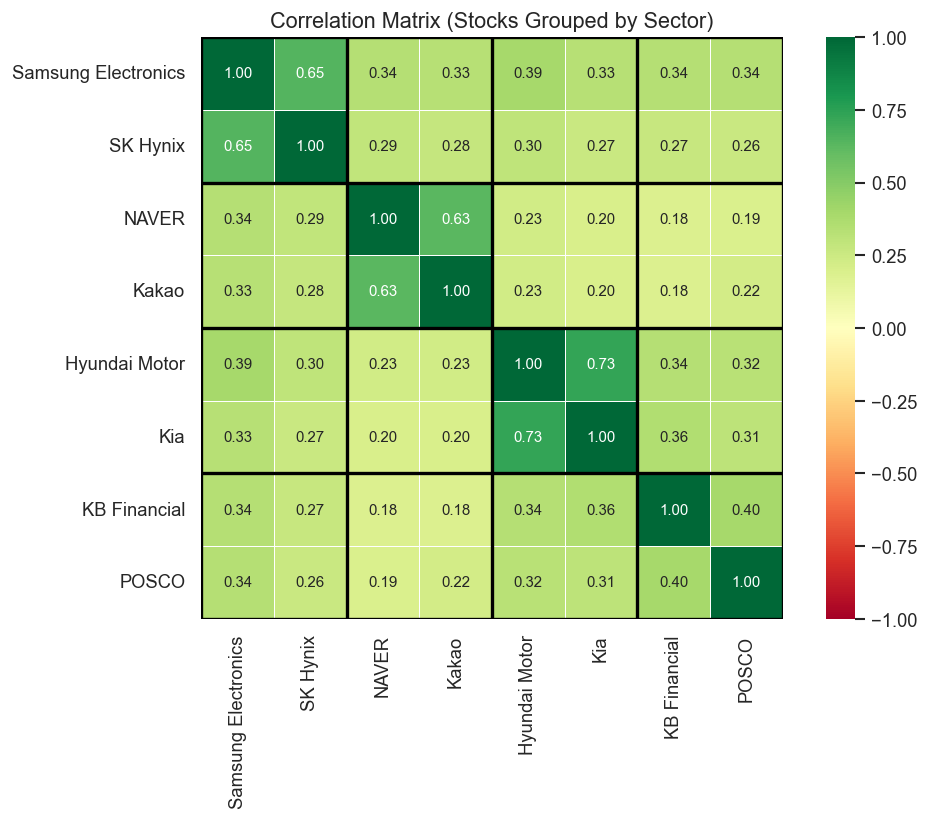

9 7. Sector-Level Analysis

9.1 7.1 Average Within-Sector vs. Cross-Sector Correlation

Code

sectors = {'Tech/Semi': ['Samsung Electronics', 'SK Hynix'],'Platform': ['NAVER', 'Kakao'],'Auto': ['Hyundai Motor', 'Kia'],'Finance/Industry': ['KB Financial', 'POSCO'],}# Build sector label for each stockstock_sector = {}for sector, stocks in sectors.items():for s in stocks: stock_sector[s] = sector# Annotated heatmap with sector groupingsordered_stocks = [s for sector in sectors.values() for s in sector]corr_ordered = returns[ordered_stocks].corr()fig, ax = plt.subplots(figsize=(9, 7))sns.heatmap( corr_ordered, annot=True, fmt='.2f', cmap='RdYlGn', vmin=-1, vmax=1, center=0, square=True, linewidths=0.5, ax=ax, annot_kws={'size': 9},)# Draw sector boundariesboundaries = [0, 2, 4, 6, 8]for b in boundaries: ax.axhline(b, color='black', linewidth=2) ax.axvline(b, color='black', linewidth=2)ax.set_title('Correlation Matrix (Stocks Grouped by Sector)', fontsize=13)plt.tight_layout()plt.show()

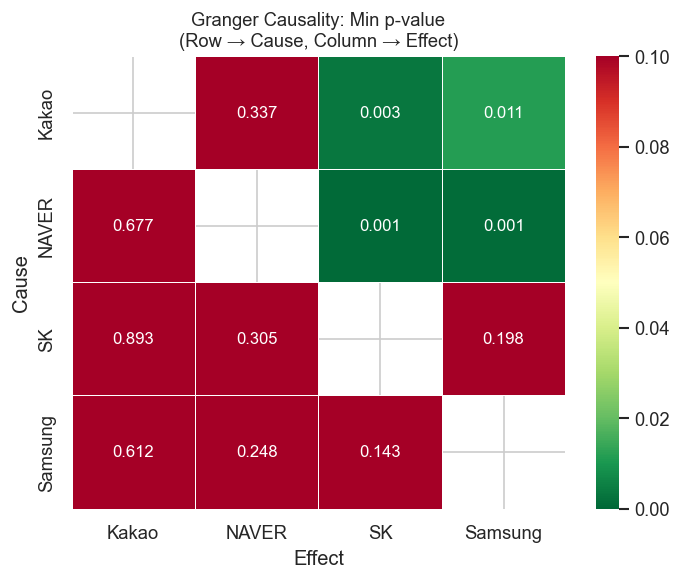

10 8. Granger Causality

Granger causality tests whether past values of stock X help predict stock Y, beyond what Y’s own past predicts. It is not causality in a strict sense — it’s predictive precedence.

Null hypothesis: X does not Granger-cause Y

Code

def granger_table(returns_df, stocks, max_lag=5):"""Return a DataFrame of Granger causality p-values.""" results = []for cause in stocks:for effect in stocks:if cause == effect:continue data = returns_df[[effect, cause]].dropna() test = grangercausalitytests(data, maxlag=max_lag, verbose=False)# use minimum p-value across lags (F-test) min_p =min(test[lag][0]['ssr_ftest'][1] for lag inrange(1, max_lag +1)) best_lag =min(range(1, max_lag +1), key=lambda l: test[l][0]['ssr_ftest'][1]) results.append({'Cause': cause.split()[0],'Effect': effect.split()[0],'Min p-value': round(min_p, 4),'Best lag': best_lag,'Significant': 'Yes'if min_p <0.05else'No', })return pd.DataFrame(results)selected_stocks = ['Samsung Electronics', 'SK Hynix', 'NAVER', 'Kakao']granger_df = granger_table(returns, selected_stocks, max_lag=5)granger_df.sort_values('Min p-value')

Cause

Effect

Min p-value

Best lag

Significant

7

NAVER

SK

0.0007

3

Yes

6

NAVER

Samsung

0.0011

1

Yes

10

Kakao

SK

0.0034

1

Yes

9

Kakao

Samsung

0.0114

1

Yes

0

Samsung

SK

0.1435

1

No

3

SK

Samsung

0.1975

2

No

1

Samsung

NAVER

0.2485

2

No

4

SK

NAVER

0.3046

2

No

11

Kakao

NAVER

0.3373

5

No

2

Samsung

Kakao

0.6116

3

No

8

NAVER

Kakao

0.6770

1

No

5

SK

Kakao

0.8934

1

No

Code

# Visualize as a heatmap of p-valuespivot = granger_df.pivot(index='Cause', columns='Effect', values='Min p-value')fig, ax = plt.subplots(figsize=(6, 5))sns.heatmap( pivot, annot=True, fmt='.3f', cmap='RdYlGn_r', # red = low p-value = significant vmin=0, vmax=0.1, linewidths=0.5, ax=ax, annot_kws={'size': 10},)ax.set_title('Granger Causality: Min p-value\n(Row → Cause, Column → Effect)', fontsize=11)plt.tight_layout()plt.show()

Caution: Granger causality in daily stock returns is hard to find due to market efficiency. Significant results are more common in intraday data or between related instruments (ETFs and their underlying stocks).

11 9. Key Takeaways

Concept

What it measures

Limitation

Pearson correlation

Co-movement at lag 0

Static; hides time dynamics

Cross-correlation function (CCF)

Co-movement at all lags

Assumes stationarity

Rolling correlation

Time-varying co-movement

Window choice is arbitrary

Granger causality

Predictive precedence

Not structural causation

Empirical findings for Korean blue chips (2018–2024):

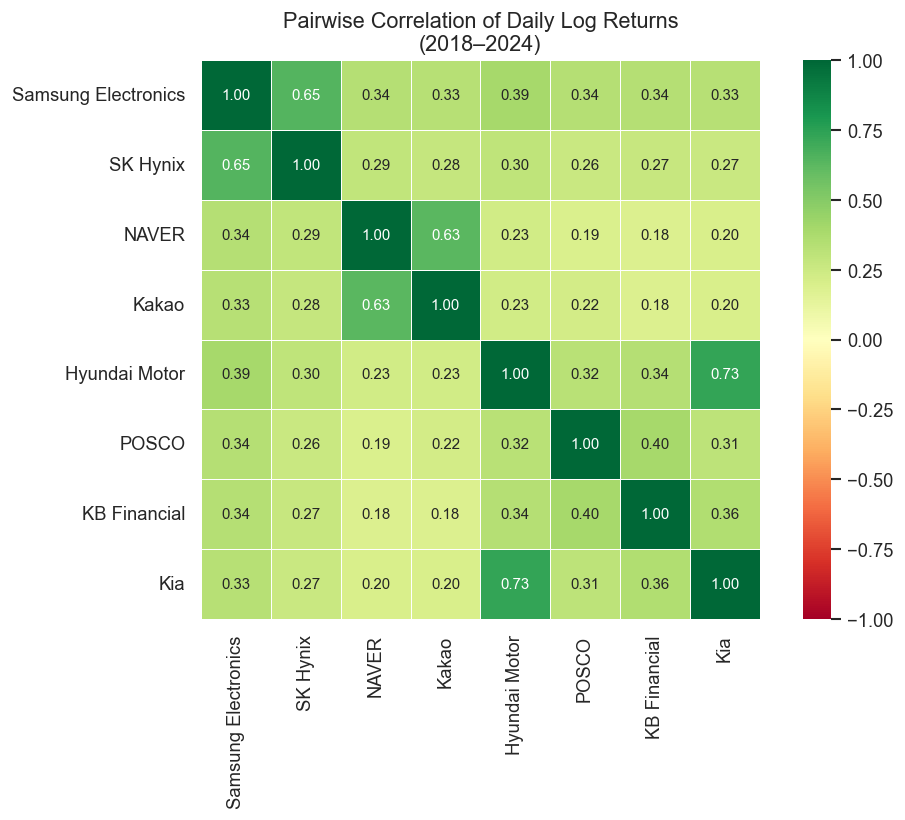

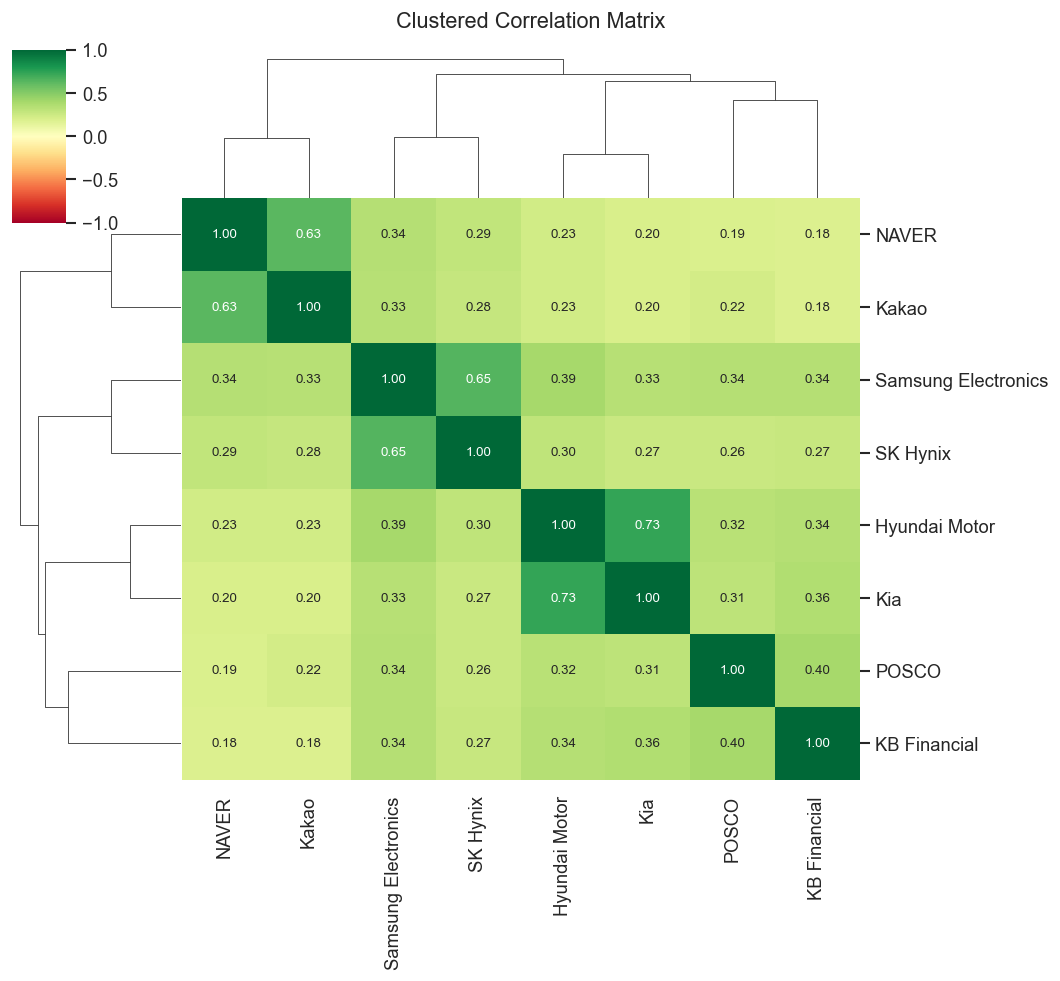

Intra-sector correlations are high: Samsung–SK Hynix (semiconductors) and Hyundai–Kia (auto) move closely together, reflecting shared business cycles and news.

Tech platform stocks (NAVER, Kakao) are moderately correlated but diverge more than the hardware pairs.

Crisis periods compress all correlations toward 1 — the diversification benefit collapses exactly when markets fall.

Lag effects are generally weak in daily data — consistent with the efficient market hypothesis.

Rolling correlations are highly non-stationary — a static correlation matrix is a snapshot, not a permanent property.

12 Next Steps

Volatility cross-correlation: Do volatility spikes (GARCH residuals) spread across stocks faster than return co-movements?

High-frequency data: Lead-lag effects are much stronger at 1–5 minute intervals

Copulas: Model non-linear tail dependence beyond linear correlation

Network analysis: Build a correlation network graph and detect communities

13 References

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The Econometrics of Financial Markets. Princeton University Press.

Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2), 223–236.

Granger, C. W. J. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica, 37(3), 424–438.